Sri Lanka banking fraud fears deepen as Kananathan warns scandals at major banks could destroy depositor and expatriate confidence.

Sri Lanka banking fraud concerns are now shaking public confidence, with Kananathan warning that depositors and expatriate remitters are being left exposed.

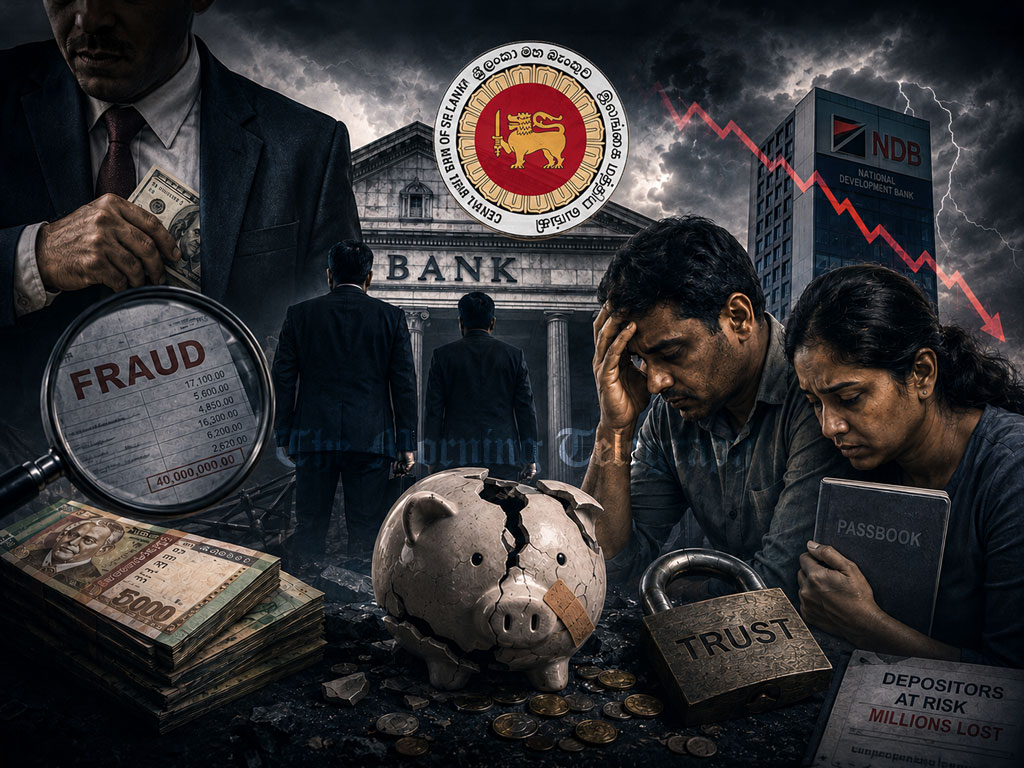

Sri Lanka’s banking sector is facing one of its gravest crises of public trust in recent memory. The unfolding fraud scandal at a private bank branch in Kandy, together with the reported disappearance of nearly USD 40 million from National Development Bank, has exposed alarming weaknesses in governance, supervision, internal controls, and regulatory accountability.

For decades, Sri Lanka’s banking industry presented itself as a stable and professionally regulated financial system. Today, that reputation has been badly damaged.

The revelations emerging from the bank scandal are deeply disturbing. According to police investigations, senior bank officials allegedly forged loan documents over several years, manipulated customer records, and siphoned millions of rupees through fraudulent transactions under the name of a long-standing customer.

The arrests of senior executives and branch management personnel suggest this was not a minor procedural failure, but a serious institutional breakdown.

Even more troubling is the allegation that repeated complaints made by the victim were ignored by the bank’s higher management. If true, this raises a serious question: was this merely negligence, or was there a deliberate attempt to suppress and conceal fraudulent activity?

The Government Analyst’s confirmation that forged documents were used by bank officials is devastating for the credibility of the institution.

Customers place their life savings in banks because they believe strict controls, audits, and regulatory safeguards exist to protect them. That trust has now been fundamentally shaken.

The situation becomes even more alarming when viewed alongside the reported massive fraud at NDB Bank, involving approximately USD 40 million.

Such an extraordinary financial disappearance cannot be dismissed as an isolated operational issue. These are failures occurring at the heart of the banking system itself.

In any serious financial jurisdiction, scandals of this magnitude would immediately trigger regulatory accountability, emergency reviews, parliamentary scrutiny, and resignations at the highest executive levels.

The Central Bank of Sri Lanka cannot escape responsibility by claiming that audits are solely the duty of commercial banks or external auditors. That argument is no longer acceptable to the public.

The Central Bank is the supreme supervisory authority of the banking sector. Its role is not ceremonial.

Its responsibility is to continuously monitor, inspect, regulate, detect irregularities, and intervene before catastrophic frauds occur.

Supervision cannot be limited to issuing circulars and conducting routine meetings while systemic failures develop unchecked beneath the surface.

When frauds involving millions of dollars emerge from leading banks, the public has every right to ask where the regulatory inspections were.

Where were the risk assessments?

Where were the warning systems?

How could such large-scale manipulation continue undetected for years?

These are not small accounting discrepancies. These are scandals that threaten confidence in the entire financial system.

What makes the situation even more damaging is that such large-scale banking frauds are extremely rare in more tightly supervised banking environments.

Sri Lanka’s financial system now risks being viewed internationally as vulnerable, weakly supervised, and internally compromised.

The implications go far beyond domestic banking operations.

At a time when the Sri Lankan government is aggressively encouraging expatriate Sri Lankans to remit foreign currency through official banking channels, these scandals send exactly the wrong message to overseas workers and investors.

Foreign remittances are one of the country’s most critical sources of foreign exchange and economic stability.

The government is trying hard to attract foreign remittances, while millions of expatriate workers sacrifice enormously to send their hard-earned income back home through the banking system.

However, when headlines are dominated by allegations of forged documents, internal collusion, and multi-million-dollar frauds inside major banks, confidence among overseas Sri Lankans will inevitably weaken.

Many expatriates may begin questioning whether their money is truly safe inside the formal banking system.

Others may divert remittances through informal channels or delay inward transfers altogether.

Such an erosion of confidence could carry serious economic consequences for a country already struggling with foreign exchange pressure and financial instability.

Confidence is the foundation of banking.

Once public trust begins to collapse, the consequences can spread rapidly across the economy.

Depositors become fearful. Investors lose confidence. International credibility deteriorates. The damage extends far beyond one institution.

Professional accountability must now begin at the top.

The CEOs and senior management of the banks implicated in these scandals cannot continue as though nothing has happened.

In any institution that values corporate governance and professional ethics, leadership must accept responsibility for catastrophic failures that occur under its watch.

Whether they had direct involvement or not is secondary to the principle of accountability.

The failure of oversight itself is sufficient grounds for resignation.

The chief executive officers and senior leadership connected to these institutions should immediately step down pending full independent investigations.

Sri Lanka cannot restore confidence in its banking system through silence, excuses, or internal damage-control operations.

Only transparency, criminal accountability, independent forensic investigations, and leadership responsibility can begin to repair the immense damage already done.

The country now faces a defining moment: either reform banking supervision with urgency and seriousness, or allow public trust in the financial sector to erode even further.