Iran frozen assets worth tens of billions remain trapped abroad. Here is where the money is held and why unlocking it matters for Tehran.

Iran frozen assets have become one of the most debated and complicated issues in relations between Tehran and the West. Unlocking the money is a key part of the recent understanding signed with the United States aimed at ending the war between the two countries.

Tehran has long sought access to money held overseas. Sanctions and banking restrictions have made much of it inaccessible. Although most Iranian assets are not physically held in the United States, Washington has significant influence over decisions that could allow Iran to access them.

Experts say releasing even part of the money could offer a critical lifeline to Iran’s battered economy. Years of sanctions, economic isolation, rising inflation and currency devaluation have taken a heavy toll. Recent conflict damage involving the United States and Israel has added further pressure.

However, experts warn that turning any political agreement into actual financial transfers will be slow and difficult. Legal, financial and political barriers remain.

What Are Iran Frozen Assets?

The total value of the assets has never been officially disclosed. However, estimates range from US$27 billion to US$100 billion.

The money does not sit in one account that Iran can simply access. Instead, it includes revenues from fuel sales and oil, gas and electricity exports. The total also includes foreign exchange reserves in overseas banks and assets trapped in legal disputes, some stretching back decades.

When Iran sells fuel abroad, buyers typically deposit payments into accounts in the purchasing country. However, sanctions have often prevented Tehran from bringing those revenues home.

The first major wave of asset freezes followed the 1979 hostage crisis at the US embassy in Tehran. A later agreement released some assets. However, claims and assets linked to military contracts signed before the 1979 Islamic Revolution remain unresolved.

A second major wave followed severe sanctions imposed in 2011 and 2012 over Iran’s nuclear programme. Those measures blocked Iran’s access to parts of the international banking system.

Restrictions tightened further after the United States withdrew from the 2015 nuclear agreement, known as the JCPOA, in 2018.

As restrictions increased, more Iranian revenue became trapped overseas. Authorities formally froze some funds, while strict conditions limited the use of others.

According to Fredrik Schneider, an economist at the Council on Global Affairs for the Middle East, there are “various forms of freezes.” These include formally blocked assets, revenues that Iran cannot repatriate and money caught in continuing legal disputes.

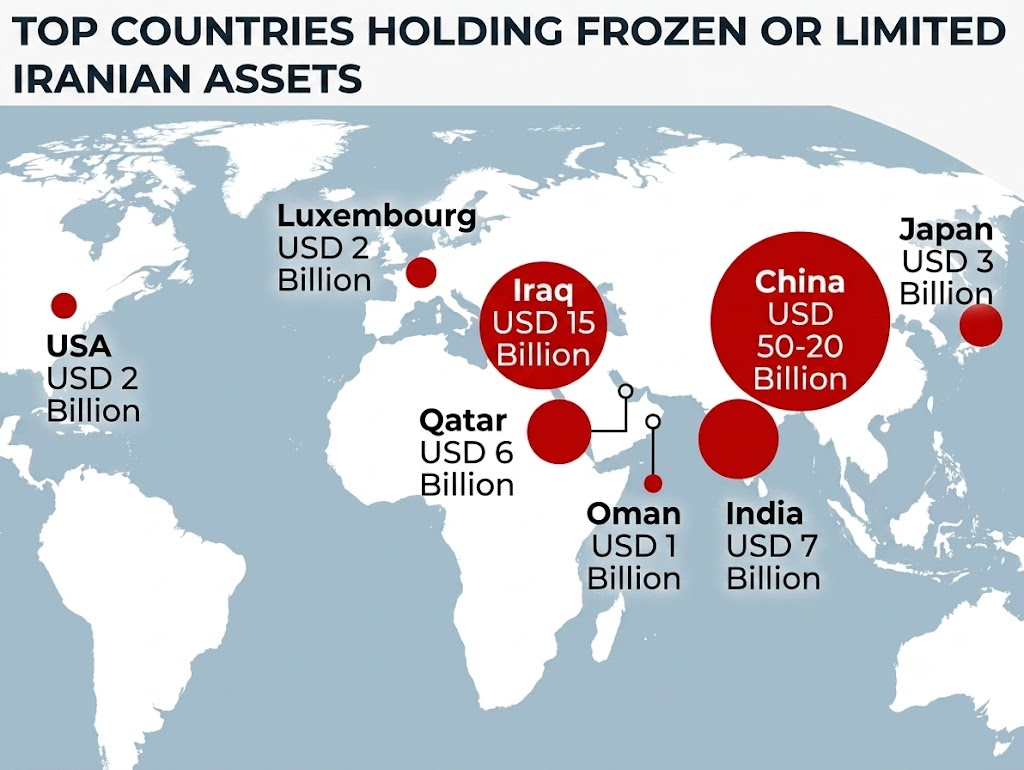

Where Are Iran’s Billions Held?

Most Iran frozen assets are located outside the United States.

China, Iran’s largest oil customer, holds a significant share. Estimates place the amount at between US$20 billion and US$50 billion.

Iraq also holds major Iranian revenues linked to payments for gas and electricity exports. Estimates put the value of those funds between US$10 billion and US$15 billion.

According to US Congressional statistics, around US$6 billion in Iranian oil revenues had been held in South Korea. Authorities transferred that money to accounts in Qatar in 2023.

However, Washington later said Iran would not gain access to the funds in the near future. The money remains in Doha.

Other Iranian funds are held in countries including India, Japan and Luxembourg.

In contrast, the amount of Iranian assets under direct US control is relatively small. According to the US Congress, the figure is approximately US$2 billion.

Much of that money is linked to court judgments and compensation claims. As a result, releasing it would be particularly difficult and politically sensitive.

Why Washington Has So Much Influence

Although most of the money sits outside the United States, Washington’s influence largely comes from secondary sanctions.

These measures target not only Iran but also foreign banks, businesses and governments that deal with it. Banks or financial institutions that help move Iranian money could lose access to the US financial system. They could also face sanctions or other penalties.

Therefore, countries holding Iranian money often hesitate to release or transfer it without clear approval from Washington.

The document outlines two main forms of economic relief for Tehran.

The first involves exemptions allowing Iran to export oil and petroleum products. It would also cover related services, including shipping, insurance and banking.

The second involves access to frozen or restricted funds. This would give Iran’s central bank greater control over how it uses the money.

The document also proposes a wider reform programme worth at least US$300 billion. The plan would seek to rebuild and develop Iran’s economy with regional partners.

The parties would implement the programme under a mechanism agreed as part of a final deal.

The United States has stressed that it is not directly paying Iran. Instead, the plan focuses on investment in infrastructure, energy, transport and other sectors.

Will Iran Actually Get the Money?

In practice, Iran may still face major restrictions when trying to access its money.

Esfandyar Batmanghelidj, founder of the UK-based Bourse & Bazaar Foundation, says these arrangements face “very complex hurdles.”

He told the BBC that Iran might be able to spend money inside a particular country. However, transferring those funds internationally could remain difficult.

Schneider points to another deeper problem: uncertainty about how long any agreement will survive.

Congress has codified some US sanctions into law. Therefore, a president cannot unilaterally remove all of them. A president can only offer temporary relief from certain restrictions.

Schneider also raised doubts about how long any relief would last. A similar pattern followed the 2015 nuclear deal. Iran regained access to some funds, but many international banks remained cautious. Then, in 2018, the United States reimposed sanctions.

Last week, Iranian state media reported that Washington had agreed to release US$12 billion in frozen assets. However, the United States has not confirmed the claim.

Questions also remain over whether Washington could use part of Iran’s assets to compensate Gulf states for war-related damage.

In early June, US Treasury Secretary Scott Bessent wrote on X that such losses “will be paid from funds seized from Iranian accounts.”

Iran rejected the proposal.

Deputy Foreign Minister Kazem Gharibabadi said Iran’s assets “are not war booty for Washington to pay its allies.”

What Could The Money Mean For Iran?

According to the World Bank, Iran’s economy was worth approximately US$475 billion in 2024.

Iranian officials have estimated war-related economic losses at up to US$300 billion. Meanwhile, the economy could contract by around 10% this year.

Releasing even part of the Iran frozen assets could provide immediate short-term relief.

A member of the Iranian Chamber of Commerce told the BBC that the shortage of foreign currency has “halted or caused long delays for many orders, with imports limited to essential goods and food.”

Experts say access to billions of dollars in foreign currency could help stabilise the Iranian rial. It could also help finance imports, including essential goods, and reduce pressure on financial markets.

However, they warn that access to money alone cannot solve Iran’s deeper structural economic problems.

Professor Kamran Naderi of Tehran’s Imam Sadiq University argues that “any reform program must prioritize controlling inflation and addressing the cost-of-living crisis.”

Without broader reforms, injecting additional money into the economy could weaken the long-term benefits of releasing the funds.

Professor Mehrdad Vahabi of Paris 13 University argues that Iran faces an even wider challenge. He points to the “sharp decline in investment and industrial obsolescence” over the past two decades.

“You cannot invest without economic security. Without real investors, Iran’s economy cannot thrive, and economic development could stagnate,” he argues.

Researcher Reza Talebi of the University of Leipzig in Germany agrees that reducing tensions will be essential. Investors need confidence that political and security risks will not endanger their money.

“The uncertain situation between war and peace is the biggest obstacle to capital entering the economy,” he adds.

Ultimately, access to Iran’s overseas money could ease immediate pressure on the rial, imports and financial markets. However, experts argue that lasting recovery will depend on more than releasing frozen billions. Economic stability, lower inflation, investment security and reduced political tensions will determine whether short-term financial relief can produce sustainable growth.