By Marlon Dale Ferreira

A single bidder. A last-minute rule change. And a decision that quietly wiped out more than USD 750,000 in enforceable penalties. What appears on the surface to be a routine crude oil deal is now raising serious questions about how contracts are awarded, altered, and approved at the highest levels. As details emerge, this tender is beginning to look less like a commercial transaction, and more like a case study in how public funds can slip through the cracks.

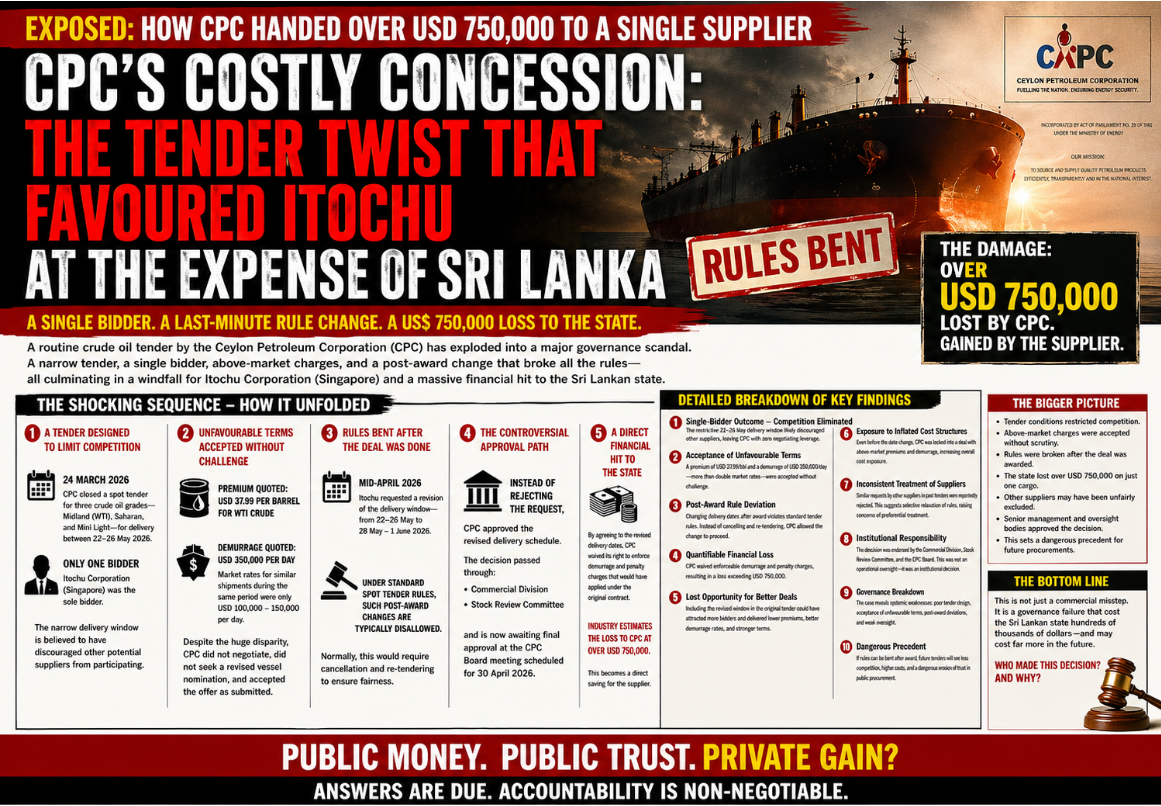

A seemingly routine crude oil procurement by the Ceylon Petroleum Corporation (CPC) has now erupted into a case that raises disturbing questions about governance, accountability, and whether public funds are being safeguarded—or quietly surrendered.

At the heart of this unfolding controversy lies a tender that drew just one bidder, a set of commercial terms that defied market logic, and a post-award decision that effectively handed over more than USD 750,000 to a foreign supplier without resistance.

And the deeper one looks, the more troubling the picture becomes.

A Tender That Never Had a Chance to Compete

On 24 March 2026, CPC closed a spot tender for three crude oil grades, Midland (WTI), Saharan, and Miri Light, with delivery scheduled between 22 and 26 May 2026.

In a global market teeming with suppliers, traders, and oil majors, the outcome should have been competitive.

Instead, only one bidder emerged, Itochu Corporation (Singapore).

This alone should have triggered alarm bells.

Industry insiders point to the tight delivery window as a likely deterrent, effectively shutting out other potential participants who may not have been able to mobilize vessels within such a narrow timeframe.

In essence, the tender structure itself appears to have restricted competition before the process even began.

A Deal Accepted on the Supplier’s Terms

With no competing bids, CPC’s negotiating leverage was already compromised. Yet what followed was even more concerning.

Itochu quoted:

- A premium of USD 37.99 per barrel for WTI crude

- A demurrage rate of USD 350,000 per day

To put this into perspective:

- For context, demurrage rates for Murban crude shipments, although a different grade from what was procured, typically range between USD 100,000 and 150,000 per day. While not directly comparable, this benchmark highlights the significant gap between prevailing market levels and the rate accepted in this instance.

That means CPC accepted a demurrage rate more than double, sometimes triple, the market norm.

Under standard procurement practice, such terms would trigger:

- Renegotiation

- Requests for alternative vessels

- Or outright rejection

Instead, CPC accepted the offer without seeking revision or challenge.

The Moment Rules Were Bent

If the initial acceptance raised eyebrows, what happened next shattered procurement norms altogether.

In mid-April 2026, Itochu requested a revision of the delivery window, from 22–26 May to 28 May–1 June 2026.

Under spot tender rules, such post-award changes are generally prohibited.

Why?

Because:

- They alter the fundamental basis of the contract

- They undermine fairness

- They disadvantage suppliers who were excluded earlier

In most systems, such a change would require:

Cancellation

Re-tendering

But CPC chose a different path.

The revised delivery window was:

- Approved by the Commercial Division

- Cleared by the Stock Review Committee

- Sent to the CPC Board for final approval

A USD 750,000 Decision

The consequences of that decision were immediate, and costly.

By agreeing to the revised delivery dates, CPC:

- Waived its right to enforce demurrage charges

- Forfeited contractual penalties for delay

Estimated financial impact:

Loss to CPC: Over USD 750,000

Gain to supplier: Over USD 750,000

This was not a market fluctuation or external shock.

It was a decision-driven loss, fully avoidable and contractually enforceable.

The Opportunity That Was Never Given a Chance

The implications extend far beyond the immediate loss.

Had CPC:

- Included the revised delivery window in the original tender

- Allowed broader supplier participation

The outcome could have been very different:

- Lower crude premiums

- Competitive demurrage rates

- Stronger overall commercial terms

Instead:

Competition was restricted at the start

Terms were relaxed only after awarding the contract

The result?

A single supplier secured a deal under conditions that were later made even more favorable.

Selective Flexibility?

Perhaps the most troubling element is not the decision itself—but the inconsistency behind it.

Market participants indicate that:

- Similar requests for delivery adjustments by other suppliers in previous tenders were rejected outright

If true, this suggests:

- Unequal treatment of suppliers

- Selective relaxation of procurement rules

And that opens the door to a far more serious question:

Was this simply poor judgment… or preferential treatment?

Not a Mistake, A Systemic Decision

This was not the action of a junior officer or an operational oversight.

The approval chain involved:

- CPC Commercial Division

- Stock Review Committee

- CPC Board (pending formalization)

This indicates:

The decision was deliberate

It was institutional

It carried full awareness of implications

A Breakdown in Procurement Discipline

Taken together, the facts paint a troubling picture:

- A tender designed in a way that limited competition

- Acceptance of clearly unfavorable commercial terms

- A post-award rule deviation that undermined fairness

- A quantifiable financial loss exceeding USD 750,000

- Inconsistent treatment of suppliers

- Senior-level approvals enabling the process

This is not an isolated lapse.

It is a systemic failure of procurement governance.

The Bigger Danger: A Precedent Set

The real risk is not just what was lost, but what has now been established.

If:

- Tender conditions can be changed after award

- Rules can be applied selectively

- Financial penalties can be voluntarily waived

Then:

Future tenders may attract fewer bidders

Costs may rise further

Public trust may erode completely

Final Question: Who Is Protecting the Public Purse?

At a time when Sri Lanka is battling economic pressure and fiscal constraints, even a “modest” loss of USD 750,000 carries weight.

But beyond the numbers lies a deeper issue:

Who made the decision… and why?

Because this was not just a commercial call.

It was a governance test.

And based on the facts now in the public domain, it is a test that raises serious questions about accountability at the highest levels.

This is not just a tender story.

This is a story about how systems meant to protect public money can fail—quietly, deliberately, and at a cost the country can ill afford.