By Roy Denish.

COPE scrutiny of NSB toxic loans exposes a Maldives-linked USD facility, unpaid debt, weak controls, and calls for a forensic audit.

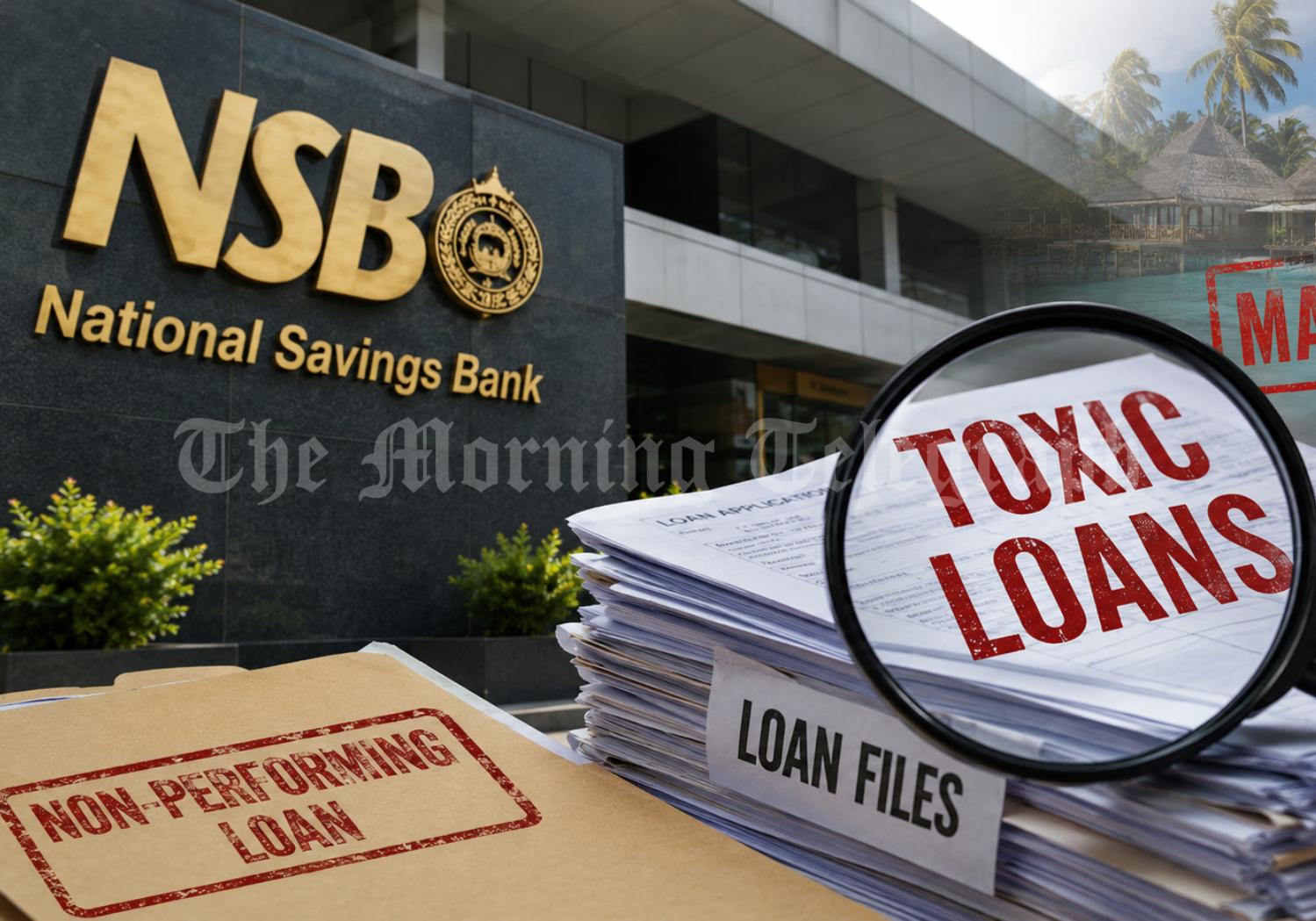

NSB toxic loans have placed the National Savings Bank under intense scrutiny after COPE exposed serious failures in credit controls, risk checks, and legal compliance.

The Committee on Public Enterprises pulled back the curtain on the bank’s credit operations and revealed a disturbing picture inside one of Sri Lanka’s key state financial institutions. At the centre of the investigation sits a large pile of non-performing loans above the five-million-rupee threshold.

According to the findings, these failed facilities have now reached a combined non-performing balance of nearly 7,972 million rupees. That figure has triggered fresh concern over the safety of public funds and the apparent ease with which credit rules appear to have been ignored.

NSB Toxic Loans Raise Questions Over Public Funds

The most controversial case involves a 9 million USD syndicated loan facility approved in June 2018 for R P I Private (Ltd), a company registered in the Maldives. NSB approved the facility jointly with the Bank of Ceylon.

COPE’s findings make the transaction especially damaging because the legal framework governing NSB strictly bars the bank from extending credit facilities to foreign companies. Yet internal governance systems failed to stop the exposure.

The situation has since worsened. The outstanding debt has climbed to 14.73 million USD, while the borrower has not repaid a single cent of the principal amount.

Investigations also found that the funds had been approved for a hotel construction project. However, the project site remains completely barren. As a result, public funds appear to have moved into a venture with no visible development and almost no physical collateral to support the exposure.

Maldives Loan Adds To Governance Crisis

The Maldives-linked loan has now become the clearest symbol of the wider NSB toxic loans controversy. It also raises deeper questions about who approved the facility, why red flags failed, and how statutory limits were bypassed.

However, the cross-border irregularity was not the only issue highlighted by the parliamentary watchdog. COPE also found serious delays in legal action against major domestic corporate defaulters.

One key example involves Bimputh Finance, a microfinance company that obtained credit facilities of 200 million rupees in 2016 and another 100 million rupees in 2019. These facilities had been backed by corporate guarantees.

Even after Bimputh Finance moved into liquidation under an order of the Colombo Commercial High Court, NSB failed to launch strong and timely recovery action. That slow response has left 258 million rupees in principal and interest unrecovered.

Another major failed facility involves Techno-Park Development Company. The company received a 750 million rupee credit facility, which has now become one of the bank’s top four failed non-performing assets. COPE’s findings have therefore sharpened criticism over the quality of NSB’s original risk assessments.

COPE Demands Forensic Audit

The pattern points to more than isolated errors. It suggests a culture of accommodation, rather than strict financial discipline.

COPE severely reprimanded the bank’s management for granting unauthorized grace period extensions to chronic, high-value defaulters. Such extensions delayed recovery action and helped hide the true scale of the toxic debt.

By allowing large corporate borrowers to default without immediate legal consequences, NSB weakened its core duty to protect public deposits. That failure now carries serious institutional consequences.

In response, COPE has called for a full forensic audit into the high-value credit lines. The committee wants investigators to trace the approval path, identify the decision-makers behind the lapses, and push for strict legal accountability.

The NSB toxic loans scandal now stands as a major test of public banking oversight. Without clear answers and firm consequences, the damage will go beyond one bank. It will deepen public suspicion over how state financial institutions manage, protect, and recover money held in trust.