Sri Lanka’s budget came tantalizingly close to a surplus in January 2026, with a gap of just 3.8 billion rupees. Tax revenues soared, and the current account turned positive. But there is a catch. The central bank depreciated the rupee, pushing up living costs. Here is the story behind the numbers and the brewing policy debate.

The latest data on the Sri Lanka budget surplus January 2026 shows that the country’s budget turned almost to surplus with a gap of only 3.8 billion rupees. This remarkable improvement came after the budget deficit collapsed in 2025, helping to turn the current account into surplus. However, at the same time, the central bank depreciated the rupee, pushing up the cost of living for ordinary citizens. This paradox of a near balanced budget alongside a weakening currency lies at the heart of Sri Lanka’s current economic policy debate and the broader discussion around the Sri Lanka budget surplus January 2026.

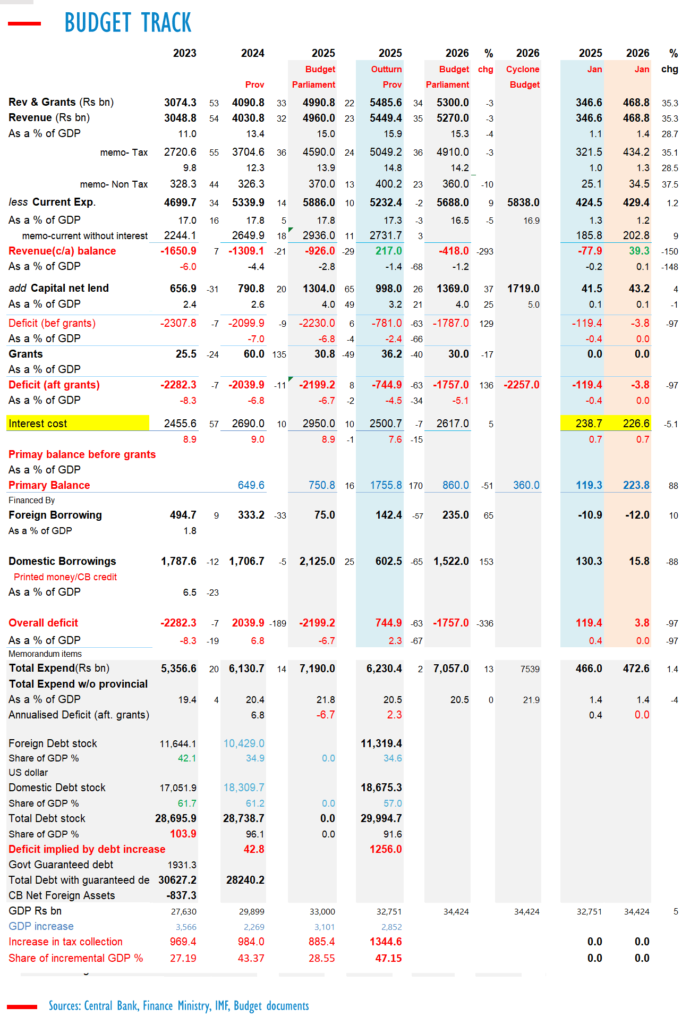

In January 2025, revenues grew 35.2 percent to 468 billion rupees. Sri Lanka tax revenues growth was particularly strong, with tax revenues rising 35.1 percent to 434 billion rupees and non tax revenue increasing 37 percent to 34.5 billion rupees. The jump in tax revenues was boosted from February 2025, when external controls were reduced to give people economic freedom, including allowing car imports to resume after a long hiatus. This move towards car imports economic freedom was seen as a relief for many households.

Blocking car imports and other highly taxed non essential goods has been a tactic used to worsen fiscal crises in the past. Critics call this a cascading policy error of macro economists who cut rates by printing money. The practice of printing money to cut rates seems to come from a belief that inflation, rather than stability, leads to growth. Yet stability is what allows businesses and individuals to plan for the long term and engage in productive investment. This misplaced belief has repeatedly led to currency depreciation that destroys capital, a lesson painfully learned during the sovereign default Sri Lanka experienced in recent years.

Recurrent spending grew just 1.2 percent to 429.4 billion rupees, helped by a net fall in interest costs. Because recurrent spending was lower than total revenues, the current account of the budget was in surplus. This aligns with the golden rule of budgeting, which says current spending should not exceed current revenue. Achieving a Sri Lanka current account surplus in the budget has been a rare feat in recent decades, and it stands as one of the few bright spots in the broader fiscal picture.

Capital expenditure was 43.2 billion rupees, up 4 percent from 41.5 billion rupees. This was almost entirely financed from current spending surpluses. However, in recent years, Sri Lanka has spent on capital projects without proper feasibility studies. This has been done to please macro economists who want a Keynesian multiplier effect from heedless spending, rather than from well designed projects that expand the country’s productive capacity and deliver permanent growth. The result has often been wasted resources and mounting debt, undermining any potential benefit from the Keynesian multiplier effect Sri Lanka desperately needs.

For the full year 2025, Sri Lanka ran a current account surplus in the budget for the first time since 1987. The overall budget deficit also collapsed to 744 billion rupees from 2,199 billion rupees a year earlier. This dramatic fiscal consolidation, reflected in the overall budget deficit 2025 figures, is one of the most significant achievements of recent economic policy. Despite this improvement, the central bank depreciated the rupee from 296 to the US dollar to 310 in 2025, raising questions about the consistency of macroeconomic management and the true causes of the cost of living increase Sri Lanka continues to face.

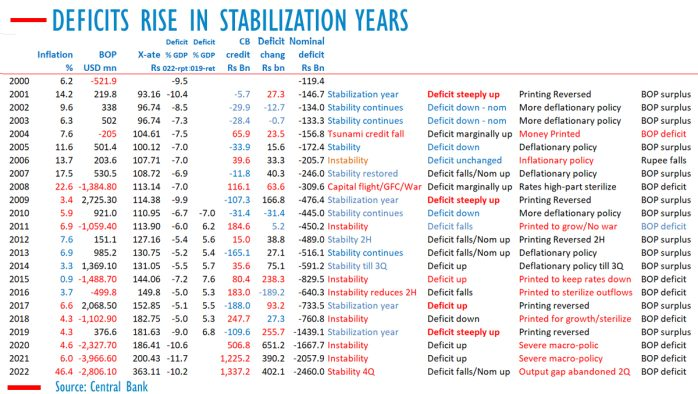

Macro economists who print money to cut rates have for decades blamed budget deficits for external trouble. They have also blamed current account deficits and twin deficits on politicians and the general public. However, analysts have shown that Sri Lanka generally has lower budget deficits in years when the central bank prints money to cut rates and trigger a currency crisis. Higher deficits appear in the year of the stabilization crisis that follows. This pattern contradicts the popular narrative about twin deficits and exposes the cascading policy error macro economists have repeatedly committed.

It has been pointed out that the narrative spread by macro economists is a spurious claim that can be easily debunked. The idea that budget deficits, rather than inflationary rate cuts meant to boost growth, are responsible for external crises and a loss of confidence in the currency does not hold up to scrutiny. In the year of stability, the correction is carried out by shrinking private credit even as the fiscal deficit rises. This is the opposite of what the standard story suggests, and it highlights how currency depreciation destroys capital more than any fiscal imbalance ever could.

There is strong opposition in Sri Lanka to central bank printing money through domestic operations. In 2025, money was printed mostly through buy sell swaps. Liquidity from dollar purchases was left unsterilized until it turned into investment and import credits. Excess liquidity at times rose close to 400 billion rupees. That is twice the level seen during the inflationary rate cuts that led to the country’s first sovereign default and a steep depreciation following a float initiated with a surrender rule in place. The memory of the sovereign default Sri Lanka endured still haunts economic policy discussions.

Sri Lanka lost the ability to run current account surpluses back in 1987. That loss came amid steep currency depreciation after budget deficits went out of control earlier in the decade, pushing nominal interest rates to very high levels. Analysts have pointed out that currency depreciation destroys capital. This leads to nominal interest rates high levels that choke off investment, and destroys budgets as current spending and capital project estimates become moving targets that are impossible to control. Once the rupee weakens, everything from food imports to debt servicing becomes more expensive.

The January 2026 budget data shows that fiscal discipline is possible. Revenue growth has been strong, and current spending is under control. But the currency remains a vulnerability. Until Sri Lanka addresses the root causes of rupee depreciation, including the temptation to print money for short term rate cuts, the cost of living will remain a burden for millions of households. The debate between those who favour stability and those who believe inflation can be a tool for growth is far from settled.